Bridging digital financial literacy gaps in the Pacific: A data-driven policy roadmap for inclusive growth

DIAN TJONDRONEGORO, AMBER MARSHALL, SHAWN HUNTER AND ELIZABETH IRENNE YUWONO |

Abstract

Digital financial literacy (DFL) is pivotal for financial inclusion and sustainable development in the Pacific Islands, yet significant disparities persist across nations. This brief introduces a four-dimensional DFL Index and applies machine learning-based clustering to analyse readiness across seven countries: Fiji, Papua New Guinea, Solomon Islands, Timor-Leste, Vanuatu, Samoa and Tonga. Findings reveal that digital skills and trust—not adoption alone—drive positive financial outcomes, with Fiji leading in readiness and other nations lagging due to infrastructure and competency gaps.

The analysis identifies three distinct clusters and highlights critical factors influencing DFL, including gender equity, cybersecurity awareness and localised education. Based on these insights, the brief proposes evidence-based policy recommendations:

- Expand rural connectivity and affordable internet access

- Deliver targeted digital financial training for women and youth

- Build trust through cybersecurity literacy and consumer protection

- Foster public–private partnerships for scalable, localised programs

By addressing these priorities, policymakers can bridge regional divides, enhance resilience and unlock economic potential in the digital era. This brief offers a strategic roadmap for inclusive digital transformation, grounded in robust data analytics and regional collaboration.

Keywords: digital financial literacy; Pacific Islands; financial inclusion; digital economy; UNCDF; machine learning; policy brief; gender equity; digital infrastructure; financial capability

Introduction

Digital financial literacy (DFL) is essential for driving economic inclusion and sustainable development. In the Pacific region, disparities in DFL highlight broader challenges related to digital infrastructure, financial education, and the trustworthiness of digital financial services (DFS). It is necessary to analyse regional trends among Pacific nations to comprehend the factors contributing to variations in DFL among their citizens. This understanding will facilitate the identification of shared challenges and provide actionable insights for policymakers to consider.

The Pacific Island nations face unique challenges related to geography, socioeconomic inequality, and infrastructure deficits, which hinder the adoption of digital and financial tools. Geographical dispersion increases the cost of connectivity, while rural and remote communities are often excluded from formal financial systems. Gender disparities further compound these issues, with women facing systemic barriers to accessing digital and financial services (Deen-Swarray et al., 2022).

This report presents a cross-country analysis of the Pacific Island nations, focusing on their shared characteristics and distinct differences in digital, traditional financial, and digital financial competencies. The goal is to represent their shared DFL characteristics and identify key factors contributing to improving DFL across these countries. The brief serves as a consideration for policymakers, aiding in creating evidence-based policy interventions to enhance DFL and support regional growth.

The 2025 UNCDF Pacific Digital Economy Programme assessed DFL regional surveys across seven Pacific Island nations: Fiji, PNG, Samoa, Solomon Islands, Timor-Leste, Tonga, and Vanuatu, providing a foundation for this policy brief (United Nations Development Programme, 2025). The survey examined four key dimensions contributing to DFL: digitalisation, traditional financial literacy, digital financial competency, and the impact of digital financial services.

The policy brief is based on a two-phase data analysis:

- Clustering analysis: This analysis groups countries based on similarities and differences in their digital and financial profiles. The method uncovers hidden patterns among multiple numeric indicators, revealing each nation’s current position in a broader financial and digital transition. These insights offer a snapshot of countries’ positions and serve as a basis for evidence-based policymaking. The optimal clustering method and number were determined based on how well-distinguished each cluster was for further analysis (further details of the analysis steps are included in Appendix A).

- Factor importance analysis: This analysis identifies the critical drivers behind high scores in each DFL dimension using machine learning techniques. It pinpoints priority areas for policy intervention by quantifying the impact of focusing on specific activities such as financial habits, digital service adoption, and the degree of digital financial knowledge. The result is determined through the lowest error in the machine learning simulation prediction, ensuring robust data-driven results (further details of the analysis steps are included in Appendix B).

The findings from the two-phase analyses illuminate the current state of each country, pinpointing potential partners and sources of insight for addressing challenges in digitalisation, finance, digital finance, and DFS impact, all to enhance DFL. These analyses establish a practical framework for policymaking; the clustering results reveal shared challenges and opportunities in the Pacific region, while the factor importance analysis indicates targeted actions to promote progress.

Utilising machine learning techniques presents several benefits for the analysis, such as the capacity to manage large datasets, reduce human errors, uncover complex relationships, and generate insights. Machine learning refers to algorithms that enable computers to recognise patterns and make data-driven decisions (Peterson et al., 2021; Sarker, 2021). This approach ensures that the findings presented in this brief are credible, robust, and firmly grounded in data, ultimately providing actionable strategies for policymakers. It highlights shared challenges, unique opportunities, and actionable solutions, offering value through:

- Regional Integration and Trends: The brief identifies common barriers and regional trends in DFL, emphasising areas where collective action is essential for impactful outcomes. It transcends the focus of individual countries to spotlight cross-border opportunities for collaboration and learning.

- Actionable Policy Recommendations: The brief is grounded in a machine learning analysis of country data, grouping nations based on characteristic patterns to identify key factors influencing high digitalisation, financial literacy, digital financial competency, and positive DFS outcomes. These findings underpin the recommended policy, offering a strategic roadmap for practical, tailored strategies.

- Focus on Inclusivity and Equity: The brief highlights interventions for vulnerable groups, such as women, youth, and rural communities, recognising the importance of equity. This ensures that DFL initiatives promote inclusive growth and leave no one behind.

- Collaboration and Knowledge Sharing: The brief underscores the importance of regional collaboration, advocating for forums and public-private partnerships to exchange best practices and foster collective progress. This collaborative approach strengthens the resilience and adaptability of Pacific Island nations in the digital financial ecosystem.

Findings and analysis

Finding 1: Shared regional challenges and opportunities

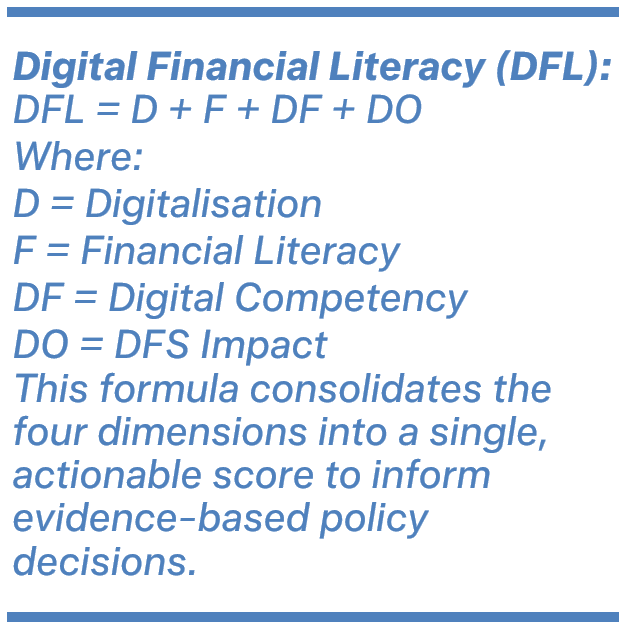

The analysis indicates that the Pacific Island countries can be grouped into three distinct clusters based on the patterns observed in their digitalisation (D), traditional financial literacy (F), digital financial competency (DF), and DFS outcomes (DO) metrics. The summation of these metrics represents the total DFL score of a country.

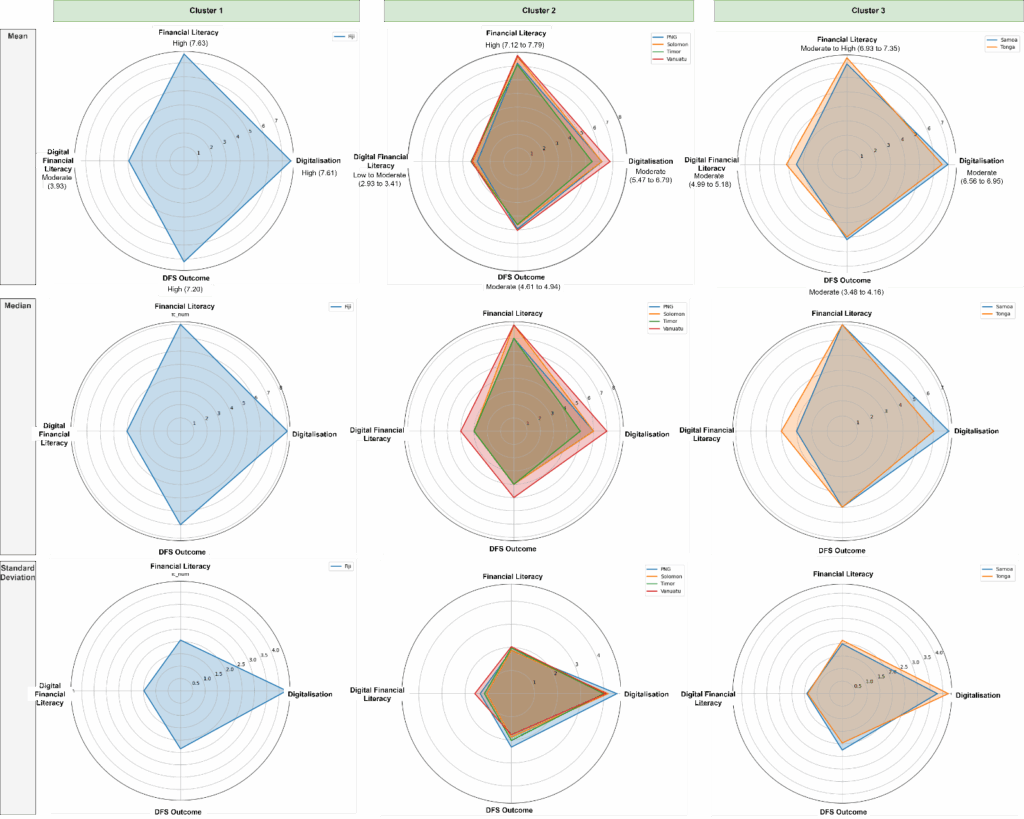

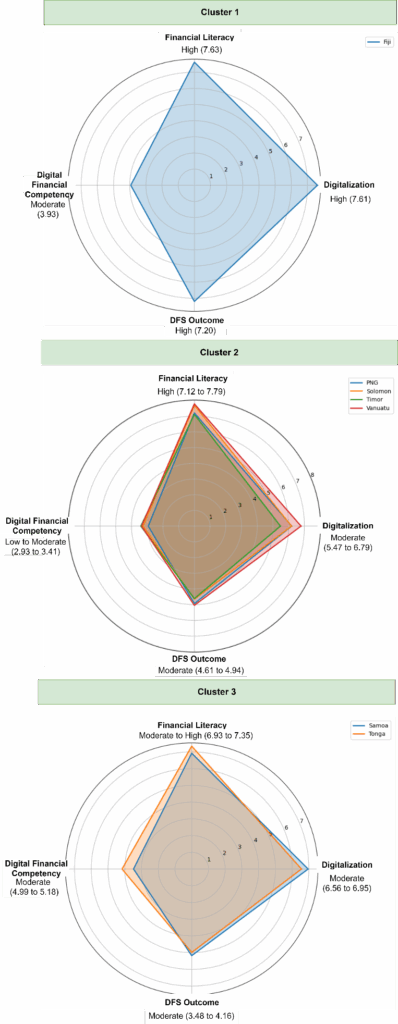

The clusters include: 1) Countries with high D, F, and DO, 2) Countries with moderate D and DO, high D, but close to the low range of DF, and 3) Countries with moderate D, DF, and DO and close to high F. Table 1 specifies the clustering results of every country represented by the average values of every category. High, moderate, and low labels are given to these values to help represent the distinction among countries and their respective cluster better. Figure 1 illustrates the difference in pattern between these clusters, with the full radar chart in Appendix C.

Table 1. Clustering of countries based on their similarities in digitalisation, financial literacy, digital financial competency, and DFS outcomes

| Clusters | Digitalisation (0 to 18) | Financial Literacy (0 to 13) | Digital Financial Competency (0 to 9) | DFS Outcome (0 to 12) |

| Cluster 1 | High (7.61) | High (7.63) | Moderate (3.93) | High (7.20) |

| Fiji | 7.61 | 7.63 | 3.93 | 7.20 |

| Cluster 2 | Moderate (5.47 to 6.79) | High (7.12 to 7.79) | Low to Moderate (2.93 to 3.41) | Moderate (4.61 to 4.94) |

| PNG | 6.19 | 7.21 | 2.93 | 4.94 |

| Solomon Islands | 6.18 | 7.70 | 3.27 | 4.65 |

| Timor-Leste | 5.47 | 7.12 | 3.41 | 4.61 |

| Vanuatu | 6.79 | 7.79 | 3.36 | 5.05 |

| Cluster 3 | Moderate (6.56 to 6.95) | Moderate to high (6.93 to 7.35) | Moderate (3.48 to 4.16) | Moderate (4.99 to 5.18) |

| Samoa | 6.95 | 6.93 | 3.48 | 5.18 |

| Tonga | 6.56 | 7.35 | 4.16 | 4.99 |

Figure 1. Radar chart of different characteristics in digitalisation, financial and digital financial literacies, and DFS outcome of the three clusters

Cluster 1: High digitalisation, high financial literacy, and high DFS outcome

This cluster is represented by high D, F, DO and moderate DF, indicating that the respondents have high competencies among other Pacific countries. This cluster is represented by Fiji respondents, who consistently have higher competency scores, although moderate DF. Fiji’s scores are distinct, and no other countries have similar characteristics. The high D, F, and DO scores (7.61, 7.63, and 7.20) indicate advanced digital infrastructure, strong smartphone penetration, broad-based financial literacy, and a strong correlation between DF and socioeconomic gains.

Fiji stands out as a leader among the Pacific Islands with its advanced mobile networks, including IoT and 5G trials. This is reflected in the 80.15 per cent of respondents acknowledging the country’s robust infrastructure and smartphone usage. While digital readiness is high in urban areas, rural regions struggle with limited infrastructure and affordability issues.

A substantial number of respondents demonstrate high financial confidence, with over half exhibiting solid financial knowledge and habits. For instance, 89.75 per cent understand what inflation means when it is discussed, 76.94 per cent of respondents regularly budget their finances, and 65.61 per cent keep track of their spending. Banking services are widely utilised in Fiji, with 62.69 per cent of people maintaining bank or credit union accounts. However, there is a noticeable gender gap in accessing financial products, as women in rural areas are 15 per cent less likely to own such products compared to men (58 per cent vs. 66 per cent). The cost of internet connectivity acts as a barrier, particularly affecting rural women and young adults.

The DFS outcomes are mainly positive. About 78.01 per cent of respondents believe that DFS will help them achieve financial security within five years, while 59.06 per cent find it easier to track their spending, which aligns with the prevalent habit of recording expenses.

Additionally, the favourable perception of DFS has positively influenced DF. Notably, 76.04 per cent see DFS as a more convenient way to receive government payments, and 63.29 per cent currently use digital wallets. Urban, younger, and higher-educated populations have higher financial and digital competencies. Nearly half of respondents expressed concern about being left behind by technology, particularly older adults, rural populations, and those with disabilities. Among these results, rural and older Fijians show lower engagement with DFS and digital tools. This disparity is further pronounced in digital financial tools like mobile wallets.

The high competency scores in this cluster are characterised by advanced infrastructure, strong traditional financial literacy, and effective conversion of digital and financial literacy into tangible socioeconomic benefits (high DO). However, the DFS usage of this cluster is primarily confined to basic transactions, with limited engagement in advanced tools like online banking and e-commerce, suggesting scope for improvement, as indicated in the moderate DF score.

Cluster 2: High financial literacy but low digital financial literacy

This cluster is marked by high F and low DFL, identified in PNG, the Solomon Islands, Timor-Leste, and Vanuatu. The D and DO in these countries are moderate, ranging from 5.47 to 6.79 for D and 4.61 to 4.94 for DO. The notable difference between the high F and low DF sets this cluster apart. The strong traditional financial knowledge in this area, similar to cluster 1, contrasts with the low DF stemming from the limited adoption of DFS. Furthermore, the moderate D and DO are reflected in survey responses, which indicate that while mobile penetration is on the rise, expensive smartphones and inadequate infrastructure in rural regions are significant barriers to wider adoption.

Analyzing the data within this cluster reveals certain correlations between D and DFS outcomes. Vanuatu demonstrates the highest D score at 6.79 among the nations evaluated, attributed to its improved internet connectivity. In contrast, Timor-Leste lags at 5.47 due to its restricted digital infrastructure and low internet penetration. This discrepancy is evident in the differences in cybersecurity habits between respondents from Vanuatu and Timor-Leste, with a 23.82 per cent variance in their practices for keeping online information safe and an 18.19 per cent difference in device virus protection. Additionally, only 10.85 per cent of Timor-Leste’s respondents own a smartwatch or speaker, and just 6.38 per cent have a smart TV, compared to 25.00 per cent and 20.02 per cent, respectively, in Vanuatu.

When it comes to DFL, PNG ranks the lowest at 2.93, mainly due to a lack of understanding of DFS. However, PNG demonstrates one of the highest rates of DFS adoption at 8.62 per cent, utilising services such as payment cards, insurance policies, and cryptocurrency. This significant adoption is also reflected in PNG’s engagement in various DFS-related activities, with an average of 21.19 per cent of individuals managing DFS passwords, using banking apps, and ensuring that websites are secure before submitting payment details. In contrast, Timor-Leste leads this group in DFL with a score of 3.41 yet has a lower overall adoption of DFS at 6.79 per cent. This difference can be attributed to Timor-Leste’s better knowledge and more positive attitudes toward DFS than other countries in this cluster. Timor-Leste has the highest DFS knowledge at 24.71 per cent, which is double that of the people in PNG. Additionally, a larger percentage of individuals in Timor-Leste, 65.6 per cent, hold a favorable view of DFS compared to 59.88 per cent in PNG. These insights indicate that a strong understanding of and positive attitude toward DFS may significantly improve DFL compared to the sheer level of DFS adoption itself.

Vanuatu leads in DO, while Timor-Leste shows the lowest DO figures, highlighting a clear correlation between D and DO. In particular, 90.76 per cent of Vanuatu’s respondents report having discretionary spending, while only 23.67 per cent of Timor-Leste’s respondents can afford personal expenses. Moreover, there is a significant 39.99 per cent gap in trust in DFS, with Vanuatu respondents demonstrating greater confidence than those in Timor-Leste.

This cluster is characterised by high F, akin to cluster 1, but with notably low DF. Countries within this group could look to Vanuatu, which showcases similar characteristics but better in D, F, and DO, to enhance their overall score. The analysis suggests that low DF correlates with lower DO due to lack of trust, affordability issues, and insufficient DFS education. This cluster highlights the relationship between D and DF in improving DO and overall score.

Cluster 3: Moderate competencies with close to high financial literacy

This cluster comprises countries with moderate scores across various categories but indicates readiness to achieve higher DF, similar to Cluster 1. The DF of this cluster ranges from 3.48 to 4.16, indicating a robust use of DFS but a lack of trust and confidence compared to Cluster 1. This cluster exhibits the lowest F scores, just below the high range of 6.93 to 7.35. Countries like Samoa and Tonga fall into this category, showing better DF than those in Cluster 2 but lagging behind Cluster 1, highlighting missed chances to capitalise on financial and digital systems.

Samoa and Tonga exhibit relatively high F, though it is not as pronounced as in other clusters. Tonga boasts a higher DF and F, leading to a better DF than Samoa. The elevated DF in Tonga primarily stems from significant DFS adoption, where the country outpaces the other by 8.08 per cent across all DFS types, especially in payment cards and digital wallets.

On the other hand, Samoa takes a slight lead with a DF score of 6.95, benefiting from greater investments in digital tools and mobile infrastructure. However, this advantage does not translate into a higher DF than Tonga. Furthermore, perceptions of DFS are notably more favourable in Tonga, with only 17.9 per cent of individuals viewing DFS as primarily for women, in stark contrast to 47.45 per cent in Samoa. It indicates a smaller gender gap in Tonga.

This cluster bridges the divide between Cluster 1 and 2 regarding D and DF, suggesting that these countries play a crucial role in boosting their national DFL. For instance, Tonga’s DF of 4.16 stands out as the highest among all countries, even surpassing Fiji from Cluster 1. This finding underscores the vital role of DF in enhancing the overall DFL index and highlights Tonga’s potential as an emerging leader in DFS adoption.

Finding 2: Key factors determining high digitaliszation, high financial, and high digital financial competencies

The second phase of the analysis focuses on the three most important factors per category. Table 2 outlines these factors with their respective importance score.

Table 2. Key factors determining high digital, financial, and digital financial competencies

| Category | Key factors | Importance score (%) |

| Digital Competency | Using formulas in a spreadsheet to make calculations | 20.63% |

| Owning a digital device i.e., a router or modem that can be used to connect devices to the internet by cable or WiFi | 7.96% | |

| Ensuring their digital device is equipped with virus protection | 7.81% | |

| Financial Literacy | Cultivating the practice of saving or investing for future needs | 59.15% |

| Having the financial knowledge that high rewards typically come with high risks | 3.28% | |

| Setting aside funds for emergencies through emergency savings | 2.20% | |

| Digital Financial Competency | Disagreeing with the notion that DFS are primarily designed for men rather than women | 17.84% |

| Verifying the security of a website before submitting payment information | 14.31% | |

| Practicing email safety by identifying suspicious emails, avoiding replies or links, and promptly deleting them to protect the security | 10.86% | |

| DFS Outcome | Benefiting from DFS in terms of simplified money management without reliance on external assistance | 16.00% |

| Enjoying the advantage of DFS for easier tracking of spending patterns | 13.31% | |

| Feeling confident about their financial security over the next five years | 10.36% |

Digital competency levels are influenced by multiple factors, with respondents’ experience in using formulas in spreadsheets accounting for a notable 20.63 per cent. Furthermore, owning a digital device for internet access, such as a router or modem, contributes 7.96 per cent to digital competency, highlighting the importance of having reliable internet connectivity. Similarly, installing virus protection on devices plays a key role, contributing 7.81 per cent. These findings suggest that digital competency is strongly linked to fundamental digital skills, internet access, and cybersecurity measures.

In the context of financial literacy, individuals who demonstrate proficiency in saving and long-term investing typically showcase a higher degree of financial literacy. This aspect is identified as the most significant factor, accounting for 59.15 per cent of overall financial literacy. Financial literacy is also influenced by 3.28 per cent of financial knowledge, particularly the understanding that higher rewards come with higher risks and 2.2 per cent is related to setting aside emergency savings. These results underscore the importance of positive habits around investment, savings, and financial education.

Awareness of secure online transactions and attitudes towards DFS are crucial to enhancing digital financial competency. DF increases when fewer individuals agree to the notion that DFS is predominantly designed for men rather than women, with a 17.99 per cent importance rating. Moreover, recognising the significance of secure online transactions when entering payment details holds 14.31 per cent importance. Practising email safety—such as identifying suspicious emails, steering clear of replies or links, and swiftly deleting any threats—accounts for 10.86 per cent of digital financial literacy. These findings suggest a need to reassess how DFS can be designed and communicated to counter perceptions of gender inequality. Competency in using online financial services is closely tied to one’s beliefs, practices, and overall behaviors.

Ultimately, positive outcomes from DFS are realised when users understand and appreciate their benefits for money management and long-term financial security. An increase in digital outcomes is seen when individuals benefit from self-reliant money management, which accounts for 16 per cent, and when they find it easier to track spending, contributing 13.31 per cent. Additionally, 10.36 per cent of positive digital outcomes stem from users feeling confident about their financial security over the next five years due to the presence of DFS. This indicates that the effectiveness of DFS relies heavily on its impact on both day-to-day and long-term money management for users.

Policy implications

DFL is crucial in advancing financial inclusion and economic empowerment in our increasingly digital landscape. It extends traditional financial literacy into the digital context, emphasising the skills and knowledge required to make informed decisions when using digital financial services (Lyons & Kass-Hanna, 2021; Ravikumar et al., 2022). Assessing a country’s DFL is important, as it is related to the country’s policymakers in establishing regulations related to access to financial services and economic participation and enhances resilience against financial risks (Widyastuti et al., 2024). A higher level of DFL empowers individuals and organisations to more fully utilise DFS, such as mobile banking, online payments, and e-commerce, which are essential in local and global economies. The following sections discuss the relevance of the findings to policymaking.

Regional trends

The analysis suggests that all countries possess high traditional financial literacy (F) but vary in their digitalisation (D), digital financial competency (DF), and digital financial services outcomes (DO). The data also show that high or low levels of digital financial competency (DF) can significantly increase and decrease citizens’ perceptions of DFS outcomes (DO) and total DFL scores. As noted earlier, the analysis reveals three groups among Pacific Island countries concerning their digital and financial capabilities:

- Fiji stands out with high digitalisation, high financial literacy, and high DFS outcomes;

- PNG, Solomon Islands, Timor-Leste, and Vanuatu show high financial literacy but low digital financial competency; and

- Samoa and Tonga exhibit moderate competencies across all four measures, with potential for growth.

As the country with the highest total score, Fiji possesses distinct characteristics compared to others. Its high digitalisation and digital financial competency indicate a correlation with the high DFS outcome and DFL score. On the other hand, low digital financial competency is observed among PNG, Solomon Islands, Timor-Leste, and Vanuatu. Analysis of this cluster also further suggests the role of digital skills in improving DFS outcomes, irrespective of the DFL score. Moderate competencies in digitalisation, financial literacy and DFS outcomes are found in Tonga and Samoa, resulting in a moderate DFL, second to Fiji. However, the role of digital financial competency in impacting the DFL score becomes more prominent in this cluster.

This finding sheds light on the crucial importance of targeted education on digital financial competency. These educational initiatives are specifically designed to enhance individuals’ understanding and responsible use of DFS. The primary objective of these programs should be to improve digital financial knowledge and attitudes by addressing critical areas, including gender inclusivity, online security, and safe digital practices. For instance, targeted educational efforts aimed at women can counter the prevalent perception that DFS predominantly serve male users. A notable illustration of this is Ethiopia’s women’s DFL campaign, which focuses on providing resources and training to empower women to confidently engage with DFS, thereby challenging the misconceptions (UNCDF, 2024). It is important for policymakers to formulate comprehensive national strategies that integrate digital financial literacy into educational curricula and public awareness campaigns. The G20/OECD-INFE Policy Guidance on Digital Financial Literacy offers a valuable framework for policymakers seeking to strengthen citizens’ DFL (OECD, 2018).

Moreover, another significant aspect of targeted education is online security and promoting safe digital financial practices. The UNCDF Policy Accelerator program exemplifies this approach through its collaboration with Saver.Global and Vodafone Fiji, which has resulted in the development of the SaverLearning platform (Wiebe, 2024). This platform encompasses modules on financial cybersecurity, significantly contributing to Fiji’s status as a leading nation in DFL within the Pacific region. The program educates users about the importance of verifying website security before submitting payment information and emphasises email safety to safeguard personal data.

Collaboration between government and financial institutions or technology providers is important to develop and distribute educational content to address the distinct needs of various demographic groups. There have been education programs delivered by mobile wallet providers where they incorporated user education into their sales strategies (Dayrit et al., 2016). However, the analysis finding in Cluster 2 (PNG, Solomon Islands, Timor-Leste, and Vanuatu) demonstrates that a high adoption rate of DFS does not necessarily equate to a high level of DFL. It indicates that many DFS users lack the requisite understanding to effectively engage with educational content or actively seek out frequently asked questions about responsible practices in the DFS educational content. A collaborative approach has been proven effective in reaching rural and low income groups in the disaster management when Cyclone Pam hit Vanuatu in March 2015, where mobile provider Digicel responded to the disaster by restoring connectivity in the capital within a few days, deploying public charging stations across the islands so that people could charge their phones and providing a total of US$250,000 free credit to their customers (Alliance for Financial Inclusion, 2017). A potential implementation could be through the ongoing Pacific Regional Education Framework (PacREF) 2018-2030: Moving Towards Education 2030 that focuses on providing equitable access to education where digital financial competency can be integrated as part of the curriculum (University of the South Pacific, 2018).

While all seven countries exhibit high financial literacy, the variation in the DFL scores suggests that high traditional financial literacy alone is not the primary determinant. This finding informs new dimensions in previous understandings of DFL, which argues that improving financial literacy can lead to better decision-making in DFL (Kumar et al., 2023). It also supports the need to treat digital finance as a distinct area requiring further educational focus (Choi et al., 2024). Additionally, it resonates with studies in developed countries demonstrating that greater experience with DFS fosters increased trust in these services (Choi et al., 2024; Powell et al., 2023).

Key considerations in improving DFL

DFL is typically evaluated using key indicators, including knowledge related to DFS, behavioural and psychological influences, socioeconomic and demographic, and digital literacy. In terms of knowledge, an individual with a high DFL understands digital tools, financial products, risk awareness, and practical application of knowledge in financial transactions (Ravikumar et al., 2022). Another indicator is behavioral and psychological influences. Previous works note that impulsivity, financial autonomy, and financial capability significantly impact financial decision-making, with financial capability mediating the link between DFL and decision-making (Kumar et al., 2023; Setiawan et al., 2022). In terms of socioeconomic factors, income, education, and access to technology, variations across gender, age, and occupation influence financial inclusion, which relates to DFL (Rehman & Mia, 2024; Widyastuti et al., 2024). Factors like marital status and employment also play roles in defining DFL levels and inclusion in digital financial ecosystems. Finally, digital skills are important in DFL, as retrieving, evaluating, and ethically using digital information and familiarity with digital platforms influence the decision-making in using DFS (Reddy et al., 2022) .

The findings highlight important factors across the competencies. Digital skills i.e., using spreadsheet formulas and increasing internet accessibility are key to improving digital competency. Financial literacy is mainly shaped by habits such as long-term saving. The role of trust in digital financial competency is underscored by behaviors focused on security in online transactions and gender perception of DFS. Positive DFS outcomes are reliant on the perceived benefits by the users of daily expense tracking and helping with long-term financial security. This finding is consistent with previous study showing that financial well-being contributes to better-informed decision-making regarding the use of DFS (Tahir et al., 2021). Additionally, it resonates with the experiential learning framework, as the practical experience of using digital tools can significantly boost literacy in digital finance (Kolb, 2014; Nimkulrat et al., 2020).

The finding suggests that enhancing overall DFL requires a holistic approach that connects technological, financial, and behavioural elements, catering to the specific needs of each country or region. One strategy could be to mobilise multi-sector task forces, such as the National Financial Inclusion Task Force, which operates across all seven countries (National Financial Inclusion Task Force, 2018). Alternatively, policymakers might consider expanding existing Financial Literacy Sub-Committees into DFL Sub-Committees, incorporating essential expertise from technology and behavioral science. For instance, the importance of being proficient in spreadsheet formulas and knowledge about DFS highlights the necessity of prioritising investments in high-quality secondary and tertiary education, particularly in the areas of science, technology, engineering, and mathematics (STEM). This emphasis is crucial for fostering the digital competencies required for effective participation in digital financial activities. Ultimately, the quality of education significantly influences DFL by equipping individuals with the essential knowledge and skills needed to thrive in an increasingly digital economy.

Policy Recommendations

This policy recommendation is derived from the issues faced by countries of similar digital and financial characteristics per cluster and cross-clusters.

Cluster-specific strategies

The recommended strategies focus on improving three clusters: digitalisation, financial literacy, digital financial competencies, and digital financial services (DFS) outcomes. Each strategy connects to key considerations for enhancing the specific area. This cross-analysis aims to show a clear path to financial and digital transformation, emphasising the most important actions to tackle challenges in these areas.

Cluster 1: Fiji, the exemplar country

For countries with strong competencies, such as Fiji, policies should focus on enhancing improving the lowest component which is DFS outcomes. This can be achieved through enhancing access to DFS in rural areas, addressing the gender gap, and improving overall perceptions of these services.

Targeted financial literacy campaigns aimed at rural women are essential for increasing account ownership and promoting DFS adoption. These initiatives will play a vital role in enhancing women’s understanding and attitudes toward DFS, thereby addressing the existing 15% gender gap in access to financial products highlighted in the findings. This approach aligns with previous notions indicating that the gender gap remains an issue even in countries with high digital financial literacy (McCosker et al., 2023; Widyastuti et al., 2024).

Furthermore, it is critical to improve DFS accessibility and infrastructure through region-specific initiatives that expand the ecosystem while ensuring security. For instance, the International Telecommunication Union’s (ITU) Smart Islands Initiative should be expanded to focus on comprehensive and cost-effective connectivity (ITU, 2023). Additionally, regional pilot programs can be introduced to integrate advanced DFS with e-commerce platforms, effectively supporting local businesses (Ge et al., 2022). Collaboration between local fintech companies and global investors should be encouraged to develop interoperable digital wallets and efficient cross-border payment solutions (Utami & Ekaputra, 2021). Promoting AI-enabled digital tools like psychometric credit assessments, chat-bots, digital data wallets and IDs and digital interactive-learning can further enhance the financial landscape. Lastly, strengthening and regulating cybersecurity and data protection measures is essential to safeguard digital financial transactions, thereby fostering trust in DFS throughout the country.

Cluster 2: Challenges facing PNG, Solomon Islands, Timor-Leste, and Vanuatu

The disparities in digital competence and financial capability within this group highlight the necessity for targeted strategies. Timor-Leste should prioritise critical investments in both infrastructure and digital literacy. Conversely, Vanuatu and the Solomon Islands can enhance their digital readiness level by expanding user-friendly DFS tools. A comparison across clusters indicates that countries in Cluster 2 must work on building trust and can gain valuable insights from the experiences of Fiji and Tonga.

The proposed policy emphasises the need to improve infrastructure and strengthen partnerships. First, infrastructure investments are crucial: extending undersea cables, such as through the South Pacific Connect initiative, and developing terrestrial networks (UNCTAD, 2024). Additionally, utilising low-orbit satellites like Starlink can help provide connectivity to remote areas, necessitating regulatory adjustments to ensure smooth integration with existing networks. The second is implementing place-based financial literacy programs tailored to local contexts (Yemini et al., 2023). These could be delivered through partnerships with banks and telecommunications providers. Moreover, promoting ICT adoption through subsidies for refurbished technology can make devices more accessible to underserved populations, ensuring they are both affordable and functional (Chen et al., 2021). Lastly, enhancing terrestrial digital infrastructure is needed to facilitate advanced digital activities and improve cybersecurity. Implementing targeted programs to raise awareness about digital financial risks and promote the use of online financial services will also be essential in boosting DFL (Aziz & Naima, 2021).

Cluster 3: High potential countries: Samoa and Tonga

Tonga’s strong digital financial capabilities position it as a potential regional leader in adopting DFS, complementing Fiji’s role. Meanwhile, Samoa can capitalise on recent infrastructure enhancements to further advance its digital service offerings. Although their digital financial competencies are superior to those in Cluster 1, there remains a significant lack of trust and confidence in digital financial services.

For such countries, policies should concentrate on leveraging existing strengths and improving the affordability of internet access. There is a need to build upon the digital readiness to promote the adoption of advanced DFS, including business tools and e-commerce platforms. In addition, policymakers need to encourage public-private partnerships to reduce data costs and expand broadband coverage in rural areas, thereby expanding access to digital tools and DFS (Lee et al., 2023).

Cross-cluster recommendations

An examination across clusters reveals significant issues related to gender disparities in financial and digital competencies, trust in DFS, and the challenges of awareness and accessibility in rural and regional areas. Although there have been notable advancements worldwide, Pacific Island nations continue to lag in DFL due to limited internet connectivity, widespread financial exclusion, and lower levels of digital trust among genders and residents in rural vs urban. For example, internet penetration is only 60% in Papua New Guinea and 57% in the Solomon Islands, while developed countries in the region is significantly higher: 93% in New Zealand and 88% in Australia (World Bank, 2020). Similarly, financial accounts ownership in nations like Timor-Leste (21%) and Papua New Guinea (40%) remains disproportionately low compared to the global average of 69% (Allen et al., 2016; UNCDF, 2023).

The gender gap is a pressing issue across Pacific Island nations, underscoring the urgent need for targeted training programs aimed at helping women in rural areas overcome systemic barriers to adopting information and communication technology (ICT) and DFS (Deen-Swarray et al., 2022). This trend is reflective of the broader gaps observed in developing countries, where disparities persist in access to and utilisation of DFS across gender, socioeconomic status, and geographic location (Tay et al., 2022).

Developed countries benefit from advanced digital and financial ecosystems characterised by high accessibility, inclusivity, and user trust in DFS (World Bank, 2020). Regulatory initiatives aimed at improving internet access, facilitating the adoption of digital tools, bridging the urban-rural divide, and enhancing digital capabilities among individuals have been instrumental in promoting digital literacy in developed countries (McCosker et al., 2023; Reddy et al., 2022). Building trust in DFS is crucial for the Pacific Islands countries ; this can be achieved through awareness campaigns highlighting the safety and reliability of mobile wallets and online banking, drawing inspiration from successful initiatives like Kenya’s mobile money service, M-PESA (Jack & Suri, 2011; McBride & Liyala, 2023).

Enhancing digital access and raising awareness about DFS in rural areas is critical. This involves strengthening digital infrastructure and promoting the adoption of digital financial services through trust-building measures and educational initiatives (Dodgson, 1993; Tay et al., 2022). The role of governments in policy formulation and regulatory measures is pivotal in expanding access to technology and fostering awareness and trust in DFS (Didenko & Buckley, 2022). Enhancing regulatory frameworks is essential to fostering competition among telecom providers while protecting local interests, thereby allowing global players such as Starlink to complement existing services (Lee et al., 2023; UNCTAD, 2024).

Moreover, regional collaboration among Pacific Island nations offers a valuable opportunity to leverage shared cultural and geographical similarities (Chatterjee et al., 2021). Establishing regional platforms can facilitate the exchange of best practices, foster partnerships, and coordinate investments in digital infrastructure. Co-designing solutions in collaboration with local organisations is a promising approach to experiential learning, ensuring that initiatives are well-aligned with the local cultural and socioeconomic context (Salmi & Mattelmäki, 2021).

Central strategies should emphasise raising awareness and enhancing literacy through community-based programs that address specific knowledge gaps in utilising DFS, particularly among underserved demographics (Setiawan et al., 2022). For instance, integrating DFL into school curriculums or community-based financial education programs has demonstrated considerable effectiveness, particularly among young adults (Choi et al., 2024; Lyons & Kass-Hanna, 2021). The financial behaviors prevalent among young adults can render them vulnerable to diminished financial well-being, as evidenced by studies on Buy Now Pay Later services in Australia (Powell et al., 2023). Furthermore, behavior-focused interventions can improve financial decision-making by addressing impulsivity and promoting long-term financial planning (Kumar et al., 2023; Tahir et al., 2021).

Conclusion

This report highlights the varying levels of digital financial readiness among Pacific island nations, underscoring the pressing need for tailored interventions to bridge existing gaps in infrastructure and literacy. Significant disparities in digital skills, financial capabilities, and digital financial expertise adversely affect these countries’ outcomes in DFS and DFL. In order to foster inclusive economic growth and enhance regional integration, it is essential to leverage Fiji’s leadership while addressing the infrastructure challenges confronted by PNG, Solomon Islands, Timor-Leste, and Vanuatu, as well as building trust in DFS across the region.

Additionally, the report outlines key activities that contribute to the advancement of DFL in the Pacific region. These activities reflect the critical importance of advanced digital experience in financial activities, cybersecurity, and DFS benefits for financial well-being in promoting inclusive economic growth throughout the Pacific Islands. Addressing the disparities in gender accessibility and the differences between rural and urban access is essential. This can be achieved through coordinated investments in technology infrastructure, education, and governance to establish more connected, equitable, and prosperous regions.

In conclusion, the recommendations presented in this policy brief offer contextual insights to guide policymakers in formulating national strategies and roadmaps to advance DFS and DFL within their countries. Gaining a thorough understanding of the current landscape of digitalisation, traditional financial literacy, and digital financial competency—through the implementation of regular DFL surveys—will provide crucial information regarding progress in this area. The identified characteristics and essential activities contributing to enhanced DFL serve as a framework for evidence-based policy and program development. This data-driven approach ensures that strategies remain responsive to the population’s evolving needs. By utilising this information, policymakers will be better positioned to evaluate their initiatives’ effectiveness and make informed adjustments, thereby promoting financial inclusion and fostering economic growth throughout the Pacific region.

Disclaimer

The views expressed in this publication do not necessarily represent those of the United Nations or its affiliated organisations. Designations and presentation of material do not imply any opinion on legal status or boundaries. In addition, the designations of country groups are intended solely for statistical or analytical convenience and do not necessarily express a judgement about the stage of development reached by a particular country or area in the development process. Reference to companies and their activities should not be construed as an endorsement by the United Nations of those companies or their activities. The boundaries and names shown and designations used on the maps presented in this publication do not imply official endorsement of acceptance by the United Nations.

Funding Statement

This work was supported by the United Nations Capital Development Fund (UNCDF) under the Pacific Digital Economy Programme (PDEP).

About the authors

Dian Tjondronegoro

Professor Dian Tjondronegoro is a Professor of Digital Business and AI Innovation at Griffith University, specialising in AI strategy, digital transformation, and responsible technology adoption across healthcare, education, and supply chain innovation. He collaborates on multidisciplinary projects in maternal–fetal health, generative AI for learning, and AI-enabled supply chains. A Fellow of the Australian Computer Society and Senior Member of IEEE and ACM, he has secured over $10M in research funding and produced 150+ publications. He advises policymakers across Asia on responsible AI and is recognised as an ACS Gold Disruptor for impactful, cross-disciplinary innovation and leadership.

Amber Marshall

Dr Amber Marshall is a Lecturer in Management at Griffith University and a member of the Griffith Asia Institute and the Centre for Work, Organisation and Wellbeing. Her research focuses on digital inclusion and rural development, examining how individuals, organisations and communities build digital capability and adopt new technologies. Using ethnographic and co-design methods, she works closely with rural and marginalised groups, including low-income families, people with disability and Indigenous communities. Amber has contributed to three ARC-funded projects and collaborated with partners such as Queensland Government, Australia Post and The Smith Family, producing research that informs policy and practical community outcomes.

Shawn Hunter

Shawn Hunter is an international development practitioner and researcher with nearly two decades of experience leading economic development initiatives across the Asia–Pacific. He specialises in financial inclusion and the digital economy, with a strong commitment to fostering inclusive and sustainable growth. Shawn has worked extensively with government agencies and industry partners, including more than ten years supporting APEC-driven cooperation and capacity-building programs. His work focuses on empowering policymakers and regulators to address emerging economic challenges. He holds a PhD in Economics from Griffith University, an MBA in Global Business Management, and a BA in Geography from the University of Queensland.

Elizabeth Irenne Yuwono

Dr Elizabeth Irenne Yuwono is an academic and researcher in AI innovation and digital transformation. She holds a PhD from Griffith University and a Master of Research from Southern Cross University. Elizabeth specialises in applying quantitative and qualitative methods, as well as innovation management strategies, to address complex challenges in education and business. Elizabeth has nearly five years of experience at Griffith University, contributing to multidisciplinary research projects. Her work emphasises practical, human-centred AI adoption and cross-sector collaboration, supporting organisations to realise the full value of technological innovation.

References

Alliance for Financial Inclusion, 2017. DFS and FinTech accelerate financial inclusion in the Pacific – Alliance for Financial Inclusion. URL https://www.afi-global.org/news/dfs-and-fintech-accelerate-financial-inclusion-in-the-pacific/ (accessed 2.7.25).

Allen, F., Demirguc-Kunt, A., Klapper, L., & Martinez Peria, M. S. (2016). The foundations of financial inclusion: Understanding ownership and use of formal accounts. Journal of Financial Intermediation, 27, 1–30. https://doi.org/10.1016/j.jfi.2015.12.003

Aziz, A., & Naima, U. (2021). Rethinking digital financial inclusion: Evidence from Bangladesh. Technology in Society, 64, 101509. https://doi.org/10.1016/j.techsoc.2020.101509

Chatterjee, S., Chaudhuri, R., Vrontis, D., & Piccolo, R. (2021). Enterprise social network for knowledge sharing in MNCs: Examining the role of knowledge contributors and knowledge seekers for cross-country collaboration. Journal of International Management, 27(1), 100827. https://doi.org/10.1016/j.intman.2021.100827

Chen, L., Gao, X., Hua, C., Gong, S., & Yue, A. (2021). Evolutionary process of promoting green building technologies adoption in China: A perspective of government. Journal of Cleaner Production, 279, 123607. https://doi.org/10.1016/j.jclepro.2020.123607

Choi, A., Stoutland, D., & Blanco, L. (2024). An evaluation of a digital financial education program and the impact of COVID-19 on financial well-being among college students. Journal of American College Health, 72(9), 3690–3702. https://doi.org/10.1080/07448481.2023.2191142

Dayrit, M., Caparas, C., Tobias, M., Abellar, M., Creus, E., Dunstan, L., 2016. Digital Financial Services in the Pacific: Experiences and Regulatory Issues. Asian Development Bank, Manila.

Deen-Swarray, M., Gillwald, A., & Morrell, A. (2022). Bridging the gender gap in ICT access and use in Africa. Information Technologies & International Development, 18(2), 13–29.

Didenko, A. N., & Buckley, R. P. (2022). Central bank digital currencies as a potential response to some particularly Pacific problems. Asia Pacific Law Review, 30(1), 44–69. https://doi.org/10.1080/10192557.2022.2045706

Dodgson, M. (1993). Learning, Trust, and Technological Collaboration. Human Relations, 46(1), 77–95. https://doi.org/10.1177/001872679304600106

Ge, H., Li, B., Tang, D., Xu, H., & Boamah, V. (2022). Research on Digital Inclusive Finance Promoting the Integration of Rural Three-Industry. International Journal of Environmental Research and Public Health, 19(6), Article 6. https://doi.org/10.3390/ijerph19063363

ITU. (2023). Smart Islands Initiative. https://www.itu.int

Jack, W., & Suri, T. (2011). Mobile money: The economics of M-PESA. National Bureau of Economic Research Working Paper Series, No. 16721. https://doi.org/10.3386/w16721

Kolb, D. A. (2014). Experiential Learning: Experience as the Source of Learning and Development (Second Edition). FT Press.

Kumar, P., Pillai, R., Kumar, N., & Tabash, M. I. (2023). The interplay of skills, digital financial literacy, capability, and autonomy in financial decision making and well-being. Borsa Istanbul Review, 23(1), 169–183. https://doi.org/10.1016/j.bir.2022.09.012

Lee, H., Jeong, S., & Lee, K. (2023). The South Korean case of deploying rural broadband via fiber networks by implementing universal service obligation and public-private partnership based project. Telecommunications Policy, 47(3), 102506. https://doi.org/10.1016/j.telpol.2023.102506

Lyons, A. C., & Kass-Hanna, J. (2021). A methodological overview to defining and measuring “digital” financial literacy. FINANCIAL PLANNING REVIEW, 4(2), e1113. https://doi.org/10.1002/cfp2.1113

McBride, N., & Liyala, S. (2023). Memoirs from Bukhalalire: A poetic inquiry into the lived experience of M-PESA mobile money usage in rural Kenya. European Journal of Information Systems, 32(2), 173–194. https://doi.org/10.1080/0960085X.2021.1924088

McCosker, A., Parkinson, S., & Et Al. (2023). Measuring Australia’s digital divide: The Australian digital inclusion index 2023. ARC Centre of Excellence for Automated Decision-Making and Society, RMIT University, Swinburne University of Technology, and Telstra. https://doi.org/10.25916/528S-NY91

McMahon, R., Hudson, H., & Fabian, L. (2014). The First Mile Connectivity Consortium and Digital Regulation in Canada. The Journal of Community Informatics, 10(2), Article 2. https://doi.org/10.15353/joci.v10i2.2741

National Financial Inclusion Task Force, 2018. Welcome to National Financial Inclusion Taskforce (NFIT) [WWW Document]. URL http://www.nfitfiji.com/ (accessed 2.7.25).

Nimkulrat, N., Groth, C., Tomico, O., & Valle-Noronha, J. (2020). Knowing together – experiential knowledge and collaboration. CoDesign, 16(4), 267–273. https://doi.org/10.1080/15710882.2020.1823995

OECD, 2018. G20/OECD-INFE Policy Guidance on Digital Financial Literacy. OECD Publishing, Paris.

Peterson, J. C., Bourgin, D. D., Agrawal, M., Reichman, D., & Griffiths, T. L. (2021). Using large-scale experiments and machine learning to discover theories of human decision-making. Science, 372(6547), 1209–1214. https://doi.org/10.1126/science.abe2629

Powell, R., Do, A., Gengatharen, D., Yong, J., & Gengatharen, R. (2023). The relationship between responsible financial behaviours and financial wellbeing: The case of buy-now-pay-later. Accounting & Finance, 63(4), 4431–4451. https://doi.org/10.1111/acfi.13100

Ravikumar, T., Suresha, B., Prakash, N., Vazirani, K., & Krishna, T. A. (2022). Digital financial literacy among adults in India: Measurement and validation. Cogent Economics & Finance, 10(1), 2132631. https://doi.org/10.1080/23322039.2022.2132631

Reddy, P., Sharma, B., & Chaudhary, K. (2022). Digital literacy: A review in the South Pacific. Journal of Computing in Higher Education, 34(1), 83–108. https://doi.org/10.1007/s12528-021-09280-4

Rehman, K., & Mia, M. A. (2024). Determinants of financial literacy: A systematic review and future research directions. Future Business Journal, 10(1), 75. https://doi.org/10.1186/s43093-024-00365-x

Salmi, A., & Mattelmäki, T. (2021). From within and in-between – co-designing organizational change. CoDesign, 17(1), 101–118. https://doi.org/10.1080/15710882.2019.1581817

Sarker, I. H. (2021). Machine Learning: Algorithms, Real-World Applications and Research Directions. SN Computer Science, 2(3), 160. https://doi.org/10.1007/s42979-021-00592-x

Setiawan, M., Effendi, N., Santoso, T., Dewi, V. I., & Sapulette, M. S. (2022). Digital financial literacy, current behavior of saving and spending and its future foresight. Economics of Innovation and New Technology, 31(4), 320–338. https://doi.org/10.1080/10438599.2020.1799142

Tahir, M. S., Ahmed, A. D., & Richards, D. W. (2021). Financial literacy and financial well-being of Australian consumers: A moderated mediation model of impulsivity and financial capability. International Journal of Bank Marketing, 39(7), 1377–1394. https://doi.org/10.1108/IJBM-09-2020-0490

Tay, L.-Y., Tai, H.-T., & Tan, G.-S. (2022). Digital financial inclusion: A gateway to sustainable development. Heliyon, 8(6). https://doi.org/10.1016/j.heliyon.2022.e09766

UNCDF. (2023). Digital and Financial Literacy Reports for Fiji, PNG, Solomon Islands, Samoa, Timor-Leste, and Vanuatu. United Nations Capital Development Fund.

UNCDF, 2024. Campaign: Women’s Digital Financial Literacy in Ethiopia — UNCDF Policy Accelerator [WWW Document]. URL https://policyaccelerator.uncdf.org/gender-intentional-policymaking/campaign-womens-digital-financial-literacy (accessed 2.7.25).

UNCTAD. (2024). Digital Economy Report: Pacific Edition. United Nations Conference on Trade and Development. https://pacificecommerce.org/pei-project/pacific-digital-economy-report-pacific-edition-2024/

United Nations Development Programme, 2025. Pacific Digital Economy Programme [WWW Document]. UNDP. URL https://www.undp.org/pacific/projects/pacific-digital-economy-programme (accessed 11.25.25).

University of the South Pacific, 2018. Pacific Regional Education Framework (PacREF) 2018-2030. Pacific Islands Forum Secretariat.

Utami, A. F., & Ekaputra, I. A. (2021). A paradigm shift in financial landscape: Encouraging collaboration and innovation among Indonesian FinTech lending players. Journal of Science and Technology Policy Management, 12(2), 309–330. https://doi.org/10.1108/JSTPM-03-2020-0064

Vassallo, D., Vella, V., & Ellul, J. (2021). Application of Gradient Boosting Algorithms for Anti-money Laundering in Cryptocurrencies. SN Computer Science, 2(3), 143. https://doi.org/10.1007/s42979-021-00558-z

Wiebe, 2024. Vodafone Fiji’s M-PAiSA and Saver.Global Partner on Financial and Digital Literacy [WWW Document]. Saver Glob. URL https://saverglobal.com/2024/12/17/saver-global-and-vodafone-fiji-bring-cybersecurity-to-fijians-in-2025/ (accessed 2.7.25).

Widyastuti, U., Respati, D. K., Dewi, V. I., & Soma, A. M. (2024). The nexus of digital financial inclusion, digital financial literacy and demographic factors: Lesson from Indonesia. Cogent Business & Management, 11(1), 2322778. https://doi.org/10.1080/23311975.2024.2322778

World Bank. (2020). Digital Economy for Development (Digital Economy Report: Pacific Edition). United Nations Conference on Trade and Development (UNCTAD). https://www.worldbank.org

Yemini, M., Engel, L., & Ben Simon, A. (2023). Place-based education – a systematic review of literature. Educational Review, 0(0), 1–21. https://doi.org/10.1080/00131911.2023.2177260

Yoon, J. (2021). Forecasting of Real GDP Growth Using Machine Learning Models: Gradient Boosting and Random Forest Approach. Computational Economics, 57(1), 247–265. https://doi.org/10.1007/s10614-020-10054-w

Zhou, X., Liu, X., Zhang, G., Jia, L., Wang, X., & Zhao, Z. (2023). An Iterative Threshold Algorithm of Log-Sum Regularization for Sparse Problem. IEEE Transactions on Circuits and Systems for Video Technology, 33(9), 4728–4740. IEEE Transactions on Circuits and Systems for Video Technology. https://doi.org/10.1109/TCSVT.2023.3247944

Appendix A. Clustering Analysis: Method and Steps

The first phase investigates the similarities and differences in characteristics across countries using the clustering method. Clustering has been used to simultaneously analyze multiple numeric variables to identify patterns and relationships that would otherwise remain hidden. This method enables the identification of nuanced differences and similarities in the country’s profiles. The clustering starts with identifying the best clustering number and method across clustering methods: connectivity-based, centroid-based, expectation-maximisation, and density-based clustering. The silhouette score is used to select the best method and cluster numbers, representing the distinction quality between selected clusters. Clusters with the highest silhouette score are chosen, as it means that the clusters are well distinguished from each other and used for further analysis of their specific attributes. For each cluster, their D, F, DF, and DO scores are labelled based on logarithmic thresholding. This method is commonly used to define low, medium, and high thresholds in machine learning-based complex data processing, e.g., image processing and behavior analyses (Zhou et al., 2023).

Objective: To cluster countries based on four key features (d_num, f_num, df_num, do_num) using multiple clustering algorithms and select the best-performing method based on the highest silhouette scores.

| Label in Pseudocode | Representation in Report |

| d_num | Respondent’s score in digitalisation (D) |

| f_num | Respondent’s score in financial literacy (F) |

| df_num | Respondent’s score in digital financial competency (DF) |

| do_num | Respondent’s score in DFS outcome |

Step 1: Data Preparation

- Input: A DataFrame country_stats containing features (d_num, f_num, df_num, do_num) with their mean and standard deviation values.

- Select relevant features for Clustering and standardise them to ensure comparability.

Step 2: Feature Selection and Standardisation

- Use the selected features (d_num, f_num, df_num, do_num) with their mean and standard deviation values.

- Standardise the data using StandardScaler to normalise feature distributions.

Step 3: Apply Clustering Algorithms

- Test three algorithms:

- K-Means Clustering: Efficient for well-separated clusters.

- Initialise K-Means with a predefined number of clusters (n_clusters=3) and fit it to the standardised data.

- Predict cluster labels and calculate the silhouette score.

- K-Means Clustering: Efficient for well-separated clusters.

- Agglomerative Clustering: Suitable for hierarchical or nested cluster structures.

- Apply Agglomerative Clustering with the same number of clusters (n_clusters=3).

- Predict cluster labels and calculate the silhouette score.

- DBSCAN: Robust to noise, identifies clusters of arbitrary shapes.

- Use DBSCAN with adjusted hyperparameters (eps, min_samples) to detect clusters of varying density.

- Predict cluster labels and calculate the silhouette score if multiple clusters are found.

Step 3: Evaluate Silhouette Scores

- Calculate silhouette scores for each method to measure the quality of Clustering.

- Ensure DBSCAN has valid scores only if more than one cluster is detected.

Step 4: Select the Best Clustering Method

- Compare silhouette scores and choose the algorithm with the highest score as the best clustering method.

- Compare silhouette scores from all three methods.

- Select the method with the highest silhouette score as the best clustering approach.

Step 5: Assign clusters and finalise results

- Add the cluster labels from the best algorithm to the country_stats DataFrame for further analysis.

Outputs

- Silhouette scores: A metric for evaluating cluster quality for each method.

- Cluster assignments: Grouped data with cluster labels based on the best algorithm.

- Visualisation (Optional): Use clustering results for plotting and additional insights.

Appendix B. Factor Importance Analysis: Method and Steps

The second phase, informed by the first phase’s findings, investigates the key factors within every category, irrespective of the respondent’s country and demographic. This phase starts with simulating all possible feature variations and priorities in different machine learning models: Gradient Boosting, Linear Regression, and Random Forest. The best model is determined through the lowest error in the simulation prediction. Three top features of each category are extracted using SHapley Additive exPlanations values, which are used to explain the output of any machine learning model, measuring each factor’s contribution to the final D, F, and DF scores.

Step 1: Preliminary analysis using hierarchical clustering

Objective: Group features into clusters using hierarchical Clustering, visualise relationships, and identify similarities across features within each component.

- Feature selection: Features are grouped into categories like Digital Inclusion, Financial Knowledge, etc.

- Data cleaning: Replace “Don’t know” values with NaN, convert columns to numeric, and scale features for clustering.

- Hierarchical clustering: Use the Ward linkage method to group similar features and create a dendrogram for visualisation.

Step 2: Machine learning for predictive modeling

Objective: Train and evaluate machine learning models to predict a target variable within each component and determine the best-performing model.

- Preprocessing: Select features and targets, clean data, and split it into training/testing datasets.

- Train models: Train three models (Linear Regression, Random Forest, Gradient Boosting) and evaluate performance using Mean Squared Error (MSE) and R-squared.

- Model selection: Identify the best model based on MSE for further analysis.

Step 3: Feature importance and SHAP analysis

Objective: Analyse the most important features affecting the predictions for the best-performing model and visualise SHAP values for interpretability.

- Feature importance: Extract feature importance scores based on the model type.

- SHAP analysis: Use SHAP to understand how features contribute to predictions, generating summary plots for visualisation.

Step 4: Simulation analysis

Objective: Simulate changes in feature values (e.g., increasing specific features by 10%) to observe their impact on predictions.

- Modify data: Increase specific feature values by 10% for simulation.

- Predict outcomes: Use the best model to predict new outcomes based on modified data.

- Compare results: Compare simulated predictions with original predictions to estimate the impact of the changes.

Outputs

- Dendrograms: Visual grouping of features for each component.

- Model evaluation metrics: MSE and R-squared for each model.

- Feature importance: Ranked importance of features for the best model.

- Simulation results: Predicted impact of feature adjustments on target variables.

Appendix C. Radar map of clustered data